Summer 2024 Newsletter

Summertime!

We hope everyone is having a wonderful summer with family and friends. In Minnesota, the 4th of July is a nice summer mid-point, with warmer temps in the extended forecast and a little drier! In this newsletter, we’ll spend time revisiting our general principles, add some current observations and touch on the elephant in the room for 2024, election season. If you make it through all of that, our Personal Side. For long-time clients (and hopefully newer clients), our general principles shouldn’t come as a surprise. But good to revisit with the 24/7 news and social media cycle of doom and gloom we’re inundated with.

General Principles

· We are goal-focused, plan driven, long-term investors. Our portfolios are derived from and driven by your lifetime financial goals, not from any view of the economy or the markets.

· We do not believe the economy can be consistently forecasted, nor the markets consistently timed. We do not believe it is possible to gain any advantage by going in and out of the markets, regardless of current conditions.

· We therefore believe that the most efficient method of capturing the full premium compound return of equities and bonds is by remaining fully invested all the time.

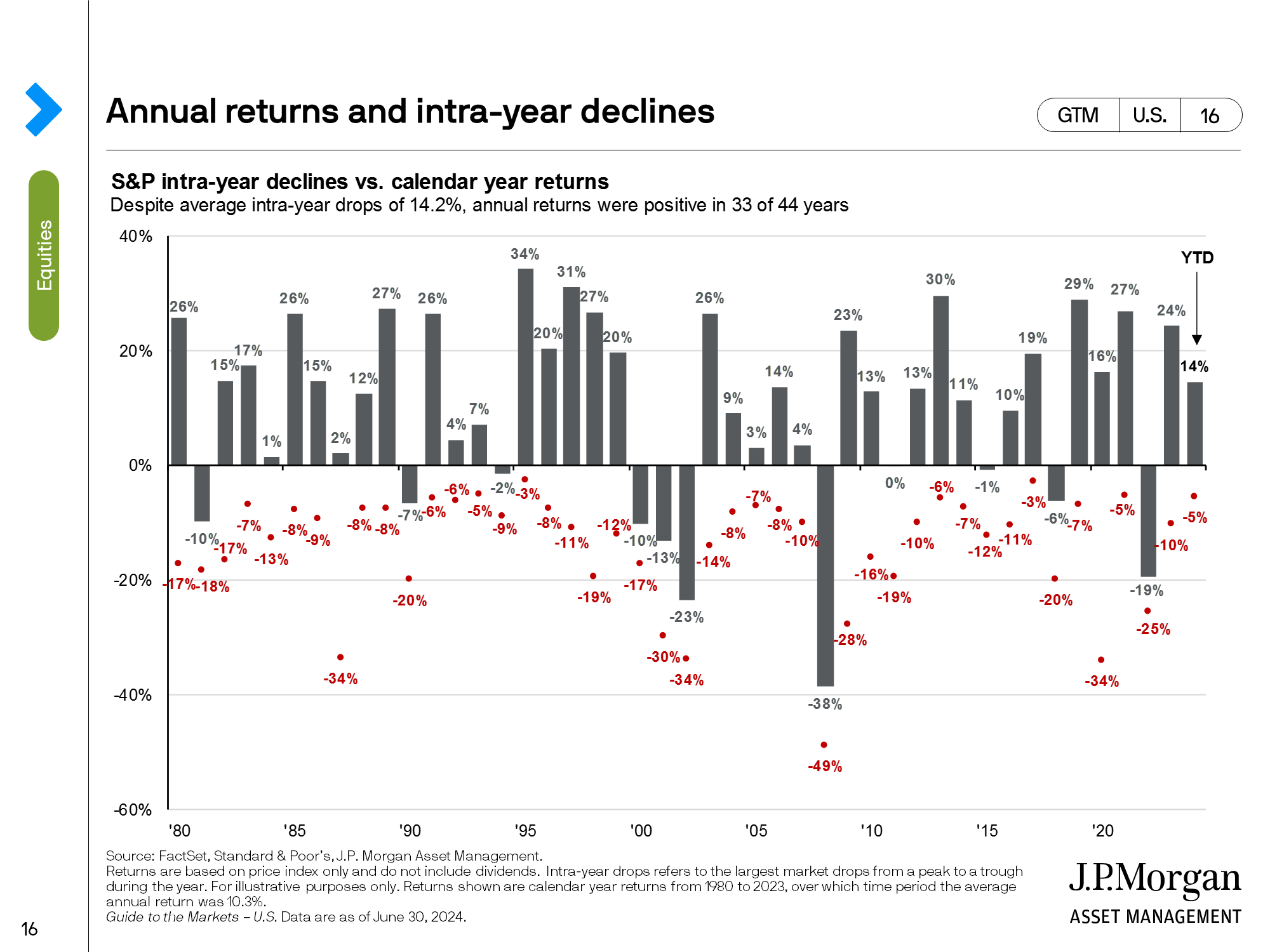

· We are thus prepared to ride out the equity market’s frequent, often significant but historically always temporary declines. We believe that even during such trying episodes, our reinvested dividends will be buying more lower-priced shares – and that the power of equity compounding will be continuing, to our long-term benefit.

First Half 2024 Commentary

The first six months of 2024 can be simply but accurately summed up in two observations. (1) The U.S. economy continued to grow, however modestly. (2) The equity market – responding to accelerating earnings growth and dividend increases, did very well. Economic growth remained marginally positive, continuing to avoid recession, while job growth continued relatively strong. Inflation slowed very grudgingly, providing the Federal Reserve with no urgent prompting to reduce interest rates. Monetary policy remains gently but quite firmly restrictive – that is, the fed funds rate is well above the inflation rate. Getting inflation down to the Fed’s target 2% remains Job One. Even without stimulating rate cuts, the equity market advanced solidly across a broad front: all three major stock indexes are significantly into new high ground. The impetus for this has been just what it fundamentally ought to be: strengthening earnings and rising dividends. Bloomberg’s current estimates are for the S&P 500’s earnings to be up 8.8% this year, to be followed by a further 13.6% increase in 2025.

Even though cash dividend payments to shareholders are at record high levels, S&P 500 companies are still paying out a below-average percentage of earnings (about 37% versus the average for the last 30 years of nearly 46%). Between that and sharply increasing earnings, there would appear to be quite a bit of room for further dividend growth this year and next. Earnings and dividends are the variables that ultimately drive the long-term value of equity market…and our ownership of equities in a broadly diversified portfolio of enduringly successful companies. Not the national debt; not the looming election; not the presence or absence of Fed rate cuts; not war(s); not the onset of the next regularly scheduled government shutdown “crisis”. Focusing on the long-term strengths of equities helps tune out the noise and lessen the danger of an emotional overreaction to gyrations in “the stock market.” And, guess what, a broadly diversified portfolio of successful companies is the best way to stay ahead of inflation.

"The farther back you can look, the farther forward you can see."

- Winston Churchill

We believe in our plan, and we like what we own. We own it too.

50 Years Ago

On July 24th, 1974, by unanimous decision, the Supreme Court ordered Richard Nixon to turn over the Watergate tapes that would ultimately end his presidency weeks later. The nation painfully endured 26 months between the Watergate break-in and the resignation of President Nixon. Some say it was the greatest constitutional crisis since the Civil War.

Throw in a roughly 50% decline in the stock market, stagflation and an oil crisis for more pain. But we persevered. Democracy persevered. Comparing today, to 50 years ago is comparing apples to oranges. But we use it as a segway to our current presidential election cycle…which for most, feels…bad.